Wavelet Analysis of Financial Data

This example shows how to use wavelets to analyze financial data.

The separation of aggregate data into different time scales is a powerful tool for the analysis of financial data. Different market forces effect economic relationships over varying periods of time. Economic shocks are localized in time and within that time period exhibit oscillations of varying frequency.

Some economic indicators lag, lead, or are coincident with other variables. Different actors in financial markets view market mechanics over shorter and longer scales. Terms like "short-run" and "long-run" are central in modeling the complex relationships between financial variables.

Wavelets decompose time series data into different scales and can reveal relationships not obvious in the aggregate data. Further, it is often possible to exploit properties of the wavelet coefficients to derive scale-based estimators for variance and correlation and test for significant differences.

Maximal Overlap Discrete Wavelet Transform — Volatility by Scale

There are a number of different variations of the wavelet transform. This example focuses on the maximal overlap discrete wavelet transform (MODWT). The MODWT is an undecimated wavelet transform over dyadic (powers of two) scales, which is frequently used with financial data. One nice feature of the MODWT for time series analysis is that it partitions the data variance by scale. To illustrate this, consider the quarterly chain-weighted U.S. real GDP data for 1947Q1 to 2011Q4. The data were transformed by first taking the natural logarithm and then calculating the year-over-year difference. Obtain the MODWT of the real GDP data down to level six with the db2 wavelet. Examine the variance of the data and compare that to the variances by scale obtained with the MODWT.

load GDPExampleData realgdpwt = modwt(realgdp,"db2",6); vardata = var(realgdp,1); varwt = var(realgdpwt,1,2);

In vardata, you have the variance for the aggregate GDP time series. In varwt, you have the variance by scale for the MODWT. There are seven elements in varwt because you obtained the MODWT down to level six, resulting in six wavelet coefficient variances and one scaling coefficient variance. Sum the variances by scale to see that the variance is preserved. Plot the wavelet variances by scale ignoring the scaling coefficient variance.

totalMODWTvar = sum(varwt);

bar(varwt(1:end-1,:))

AX = gca;

AX.XTickLabels = {"[2 4)","[4 8)","[8 16)","[16 32)","[32 64)","[64 128)"};

xlabel("Quarters")

ylabel("Variance")

title("Wavelet Variance by Scale")

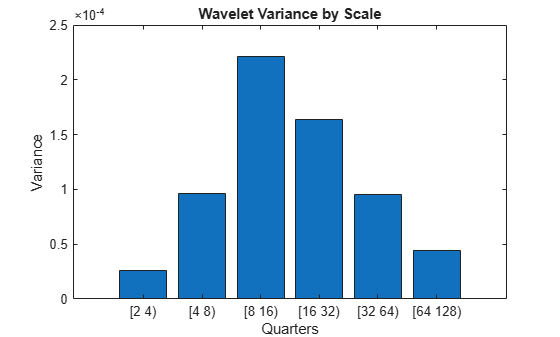

Because this data is quarterly, the first scale captures variations between two and four quarters, the second scale between four and eight, the third between 8 and 16, and so on.

From the MODWT and a simple bar plot, you see that cycles in the data between 8 and 32 quarters account for the largest variance in the GDP data. If you consider the wavelet variances at these scales, they account for 57% of the variability in the GDP data. This means that oscillations in the GDP over a period of 2 to 8 years account for most of the variability seen in the time series.

Great Moderation — Testing for Changes in Volatility with the MODWT

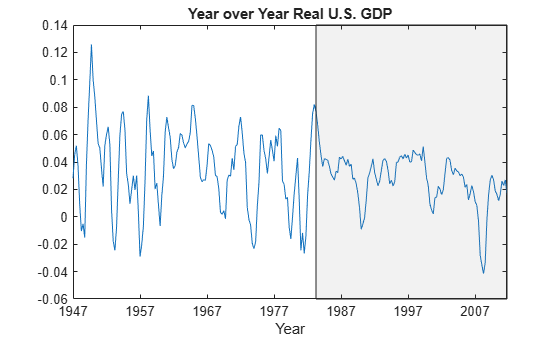

Wavelet analysis can often reveal changes in volatility not evident in aggregate data. Begin with a plot of the GDP data.

helperFinancialDataExample1(realgdp,year,"Year over Year Real U.S. GDP")

The shaded region is referred to as the "Great Moderation" signifying a period of decreased macroeconomic volatility in the U.S. beginning in the mid-1980s.

Examining the aggregate data, it is not clear that there is in fact reduced volatility in this period. Use wavelets to investigate this by first obtaining a multiresolution analysis of the real GDP data using the db2 wavelet down to level 6.

realgdpwt = modwt(realgdp,"db2",6,"reflection"); gdpmra = modwtmra(realgdpwt,"db2","reflection");

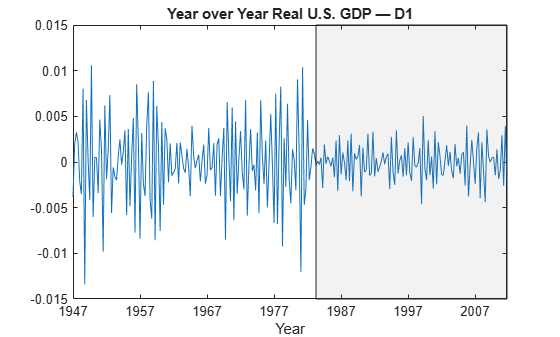

Plot the level-one details, D1. These details capture oscillations in the data between two and four quarters in duration.

helperFinancialDataExample1(gdpmra(1,:),year, ... "Year over Year Real U.S. GDP — D1")

Examining the level-one details, it appears there is a reduction of variance in the period of the Great Moderation.

Test the level-one wavelet coefficients for significant variance changepoints.

[pts_Opt,kopt,t_est] = wvarchg(realgdpwt(1,1:numel(realgdp)),2); years(pts_Opt)

ans = duration

142 yrs

There is a variance changepoint identified in 1982. This example does not correct for the delay introduced by the db2 wavelet at level one. However, that delay is only two samples so it does not appreciably affect the results.

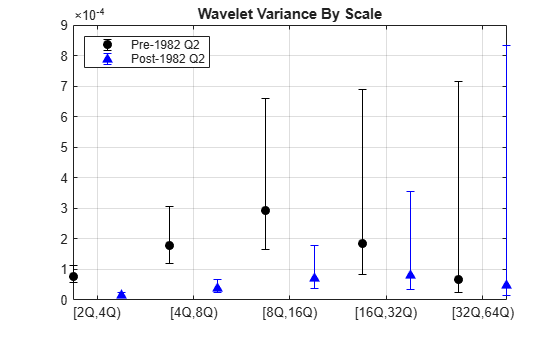

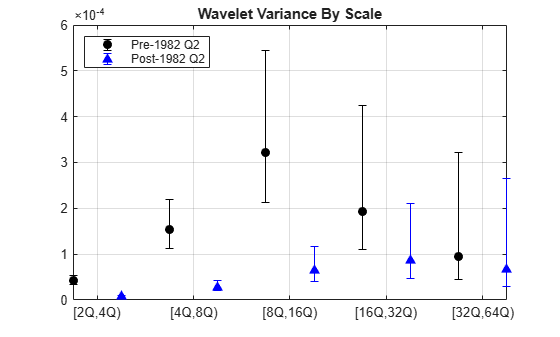

To assess changes in the volatility of the GDP data pre- and post-1982, split the original data into pre- and post-changepoint series. Obtain the wavelet transforms of the pre and post datasets. In this case, the series are relatively short so use the Haar wavelet to minimize the number of boundary coefficients. Compute unbiased estimates of the wavelet variance by scale and plot the result.

tspre = realgdp(1:pts_Opt); tspost = realgdp(pts_Opt+1:end); wtpre = modwt(tspre,"haar",5); wtpost = modwt(tspost,"haar",5); prevar = modwtvar(wtpre,"haar","table"); postvar = modwtvar(wtpost,"haar","table"); xlab = {"[2Q,4Q)","[4Q,8Q)","[8Q,16Q)","[16Q,32Q)","[32Q,64Q)"}; helperFinancialDataExampleVariancePlot(prevar,postvar,"table",xlab) title("Wavelet Variance By Scale") legend("Pre-1982 Q2","Post-1982 Q2",Location="NorthWest")

From the preceding plot, it appears there are significant differences between the pre-1982Q2 and post-1982Q2 variances at scales between 2 and 16 quarters.

Because the time series are so short in this example, it can be useful to use biased estimates of the variance. Biased estimates do not remove boundary coefficients. Use a db2 wavelet filter with four coefficients.

wtpre = modwt(tspre,"db2",5,"reflection"); wtpost = modwt(tspost,"db2",5,"reflection"); prevar = modwtvar(wtpre,"db2",0.95,"table",EstimatorType="biased"); postvar = modwtvar(wtpost,"db2",0.95,"table",EstimatorType="biased"); xlab = {"[2Q,4Q)","[4Q,8Q)","[8Q,16Q)","[16Q,32Q)","[32Q,64Q)"}; figure helperFinancialDataExampleVariancePlot(prevar,postvar,"table",xlab) title("Wavelet Variance By Scale") legend("Pre-1982 Q2","Post-1982 Q2",Location="NorthWest")

The results confirm our original finding that the Great Moderation is manifested in volatility reductions over scales from 2 to 16 quarters.

Wavelet Correlation Analysis of GDP Component Data

You can also use wavelets to analyze correlation between two datasets by scale. Examine the correlation between the aggregate data on government spending and private investment. The data cover the same period as the real GDP data and are transformed in the exact same way.

[rho,pval] = corrcoef(privateinvest,govtexp);

Government spending and personal investment demonstrate a weak, but statistically significant, negative correlation of -0.215. Repeat this analysis using the MODWT.

wtPI = modwt(privateinvest,"db2",5,"reflection"); wtGE = modwt(govtexp,"db2",5,"reflection"); wcorrtable = modwtcorr(wtPI,wtGE,"db2",0.95,"reflection","table"); display(wcorrtable)

wcorrtable=6×6 table

NJ Lower Rho Upper Pvalue AdjustedPvalue

___ ________ ________ __________ _________ ______________

D1 257 -0.29187 -0.12602 0.047192 0.1531 0.7502

D2 251 -0.54836 -0.35147 -0.11766 0.0040933 0.060171

D3 239 -0.62443 -0.35248 -0.0043207 0.047857 0.35175

D4 215 -0.70466 -0.32112 0.20764 0.22523 0.82773

D5 167 -0.63284 0.12965 0.76448 0.75962 1

S5 167 -0.63428 0.12728 0.76347 0.76392 1

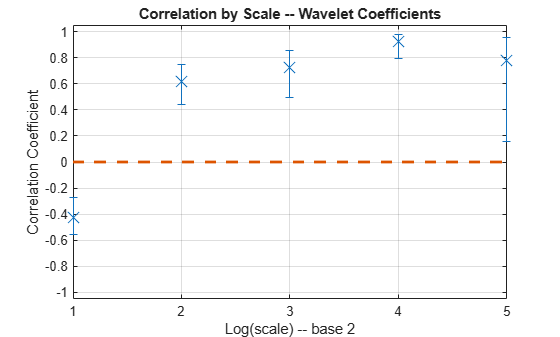

The multiscale correlation available with the MODWT shows a significant negative correlation only at scale 2, which corresponds to cycles in the data between 4 and 8 quarters. Even this correlation is only marginally significant when adjusting for multiple comparisons.

The multiscale correlation analysis reveals that the slight negative correlation in the aggregate data is driven by the behavior of the data over scales of four to eight quarters. When you consider the data over different time periods (scales), there is no significant correlation.

Wavelet Cross-Correlation Sequences — Leading and Lagging Variables

With financial data, there is often a leading or lagging relationship between variables. In those cases, it is useful to examine the cross-correlation sequence to determine if lagging one variable with respect to another maximizes their cross-correlation. To illustrate this, consider the correlation between two components of the GDP — personal consumption expenditures and gross private domestic investment.

piwt = modwt(privateinvest,"fk8",5); pcwt = modwt(pc,"fk8",5); figure modwtcorr(piwt,pcwt,"fk8")

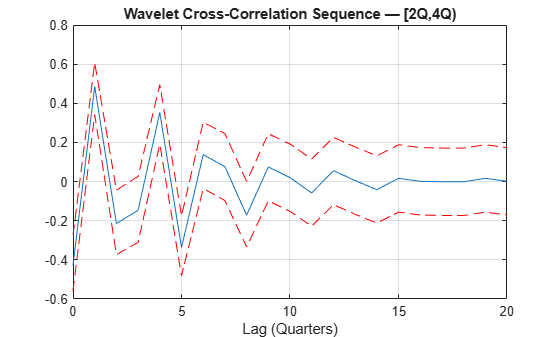

Personal expenditure and personal investment are negatively correlated over a period of 2–4 quarters. At longer scales, there is a strong positive correlation between personal expenditure and personal investment. Examine the wavelet cross-correlation sequence at the scale representing 2–4 quarter cycles.

[xcseq,xcseqci,lags] = modwtxcorr(piwt,pcwt,"fk8"); zerolag = floor(numel(xcseq{1})/2)+1; plot(lags{1}(zerolag:zerolag+20),xcseq{1}(zerolag:zerolag+20)); hold on plot(lags{1}(zerolag:zerolag+20),xcseqci{1}(zerolag:zerolag+20,:),"r--") hold off xlabel("Lag (Quarters)") grid on title("Wavelet Cross-Correlation Sequence — [2Q,4Q)")

The finest-scale wavelet cross-correlation sequence shows a peak positive correlation at a lag of one quarter. This indicates that personal investment lags personal expenditures by one quarter.

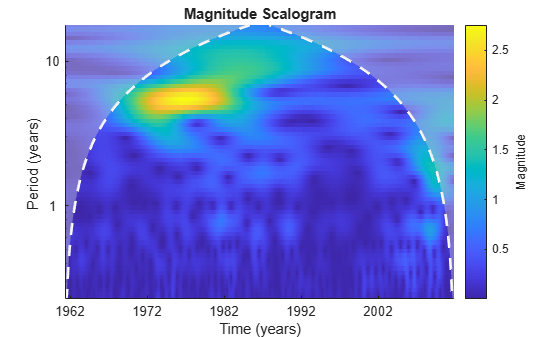

Continuous Wavelet Analysis of U.S. Inflation Rate

Using discrete wavelet analysis, you are limited to dyadic scales. This limitation is removed when using continuous wavelet analysis.

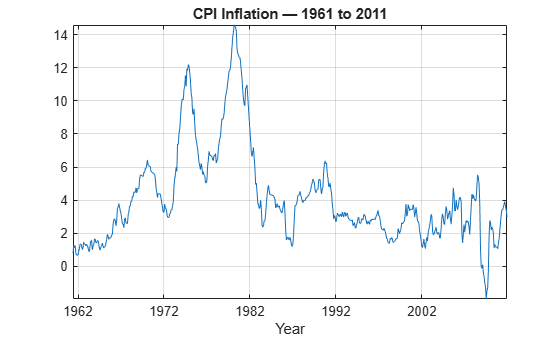

Load U.S. inflation rate data from May 1961 to November 2011.

load CPIInflation figure plot(yr,inflation) AX = gca; AX.XTick = 1962:10:2011; title("CPI Inflation — 1961 to 2011") axis tight grid on xlabel("Year")

In the time data, a slow oscillation appears in the early 1970s and seems to dissipate by the late 1980s.

To characterize the periods of increased volatility, obtain the continuous wavelet transform (CWT) of the data using the analytic Morlet wavelet.

cwt(inflation,"amor",years(1/12));

AX = gca;

AX.XTick = 8/12:10:596/12;

AX.XTickLabels = yr(round(AX.XTick*12));

The CWT reveals the strongest oscillations in the inflation rate data in the approximate range of 4–6 years. This volatility begins to dissipate by the mid 1980s and is characterized by both a gradual reduction in inflation and a shift in volatility toward longer periods. The strong volatility cycles in the 1970s and into the early 1980s are a result of the 1970s energy crisis (oil shocks) which resulted in stagflation (stagnant growth and inflation) in the major industrial economies. See [1] for an in-depth CWT-based analysis of these and other macroeconomic data. This example reproduces a small part of the broader and more detailed analysis in that paper.

Conclusions

In this example you learned how to use the MODWT to analyze multiscale volatility and correlation in financial time series data. The example also demonstrated how wavelets can be used to detect changes in the volatility of a process over time. Finally, the example showed how the CWT can be used to characterize periods of increased volatility in financial time series. The references provide more detail on wavelet applications for financial data and time series analysis.

Appendix

The following helper functions are used in this example:

References

[1] Aguiar-Conraria, Luís, Manuel M.F. Martins, and Maria Joana Soares. “The Yield Curve and the Macro-Economy across Time and Frequencies.” Journal of Economic Dynamics and Control 36, no. 12 (December 2012): 1950–70. https://doi.org/10.1016/j.jedc.2012.05.008.

[2] Crowley, Patrick M. “A Guide to Wavelets for Economists.” Journal of Economic Surveys 21, no. 2 (April 2007): 207–67. https://doi.org/10.1111/j.1467-6419.2006.00502.x.

[3] Gallegati, Marco, and Willi Semmler, eds. Wavelet Applications in Economics and Finance. Vol. 20. Dynamic Modeling and Econometrics in Economics and Finance. Cham: Springer International Publishing, 2014. https://doi.org/10.1007/978-3-319-07061-2.

[4] Percival, Donald B., and Andrew T. Walden. Wavelet Methods for Time Series Analysis. Cambridge: Cambridge University Press, 2000.