Estadística

CLASIFICACIÓN

257

of 297.589

REPUTACIÓN

350

CONTRIBUCIONES

0 Preguntas

141 Respuestas

ACEPTACIÓN DE RESPUESTAS

0.00%

VOTOS RECIBIDOS

74

CLASIFICACIÓN

437 of 20.461

REPUTACIÓN

3.736

EVALUACIÓN MEDIA

4.60

CONTRIBUCIONES

12 Archivos

DESCARGAS

213

ALL TIME DESCARGAS

29494

CLASIFICACIÓN

of 159.227

CONTRIBUCIONES

0 Problemas

0 Soluciones

PUNTUACIÓN

0

NÚMERO DE INSIGNIAS

0

CONTRIBUCIONES

26 Publicaciones

CONTRIBUCIONES

0 Público Canales

EVALUACIÓN MEDIA

CONTRIBUCIONES

0 Temas destacados

MEDIA DE ME GUSTA

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Feeds

Publicado

Modeling Exchange Rate Volatility

The following post is from William Mueller, Software Developer on the Econometrics Toolbox Team. Forecasting currency...

11 días hace

Publicado

Assessing Climate Impacts on Credit Risk

We recently hosted a technical webinar focused on climate transition risk, specifically assessing climate impacts on credit...

14 días hace

Publicado

Simplifying Econometric Modeling with MATLAB

Econometric modeling is essential for analyzing economic data, making forecasts, and informing policy decisions, however,...

18 días hace

Publicado

Celebrating 30 Years of Dynare and Its Global Impact with MATLAB

As we celebrate the 30th anniversary of Dynare, we at MathWorks would like to take a moment to reflect on its influence on...

24 días hace

Publicado

Custom Portfolio Optimization: Balancing Objectives, Constraints, and Efficiency

The following blog was written by Marshall Alphonso Principal Engineer and Sara Galante, Senior Finance Application...

alrededor de 1 mes hace

Publicado

Physics-Informed Neural Networks (PINNs) for Option Pricing

The following post is from Jue Liu from Columbia University and Yuchen Dong from MathWorks. The example featured in the...

2 meses hace

Publicado

MathWorks Secures Silver in Chartis RiskTech AI 50 and Excels in Key Categories

We are proud to announce that MathWorks has been ranked second overall in the inaugural Chartis RiskTech AI 50, an...

4 meses hace

Publicado

Accelerating Model Deployment in Financial Institutions with Automation

Today’s topic is one that’s really making waves in the financial world these days: speeding up the deployment of models...

4 meses hace

Publicado

Highlights from the MathWorks Finance Conference 2024

The 2024 MathWorks Finance Conference brought together industry leaders to explore the evolving landscape of finance...

4 meses hace

Publicado

A MATLAB Implementation of the DICE-2023 Model for Climate-Economic Analysis

The DICE (Dynamic Integrated model of Climate and the Economy) model has been a cornerstone for understanding the intricate...

4 meses hace

Publicado

Trading Analysis in MATLAB using Python DataFrames

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks. The GitHub documentation...

5 meses hace

Publicado

Modeling Carbon Emissions: An Econometric Approach

In a recent webinar hosted by MathWorks, we were joined by Andy Cates, a senior economist at Haver Analytics, one of our...

5 meses hace

Publicado

Deep Learning in Quantitative Finance: Multiagent Reinforcement Learning for Financial Trading

The following blog was written by Adam Peters, Software Engineer at Mathworks. Download the code for this example from...

10 meses hace

Publicado

Key Insights from our Executive Panel Discussion: Addressing Climate Risk through effective Stress Testing, Reporting, and Governance

Background In the rapidly evolving landscape of financial risk management, addressing climate risk has emerged as a...

12 meses hace

Publicado

MATLAB Portfolio Backtesting – A new app now on GitHub!

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks. MathWorks has a new...

alrededor de 1 año hace

Publicado

Top MATLAB Quantitative Finance Resources now on GitHub

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks. MathWorks now has a...

alrededor de 1 año hace

Publicado

Model Monitoring and Drift Detection with Modelscape

MathWorks recently hosted a webinar on Model Monitoring and Drift Detection, where Paul Peeling presented strategies for...

alrededor de 1 año hace

Publicado

Deep Learning in Quantitative Finance: Transformer Networks for Time Series Prediction

The following blog was written by Owen Lloyd , a Penn State graduate who recently join the MathWorks Engineering...

alrededor de 1 año hace

Publicado

Climate Risk in Finance: Insights from Our Comprehensive Executive Panel Discussion

The following blog was written by Arpit Narain from the MathWorks Finance team. 1. Introduction In today’s financial...

alrededor de 1 año hace

Publicado

Managing and Fine-Tuning Portfolio Optimization Workflows with Experiment Manager

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks. The code used to develop...

más de 1 año hace

Publicado

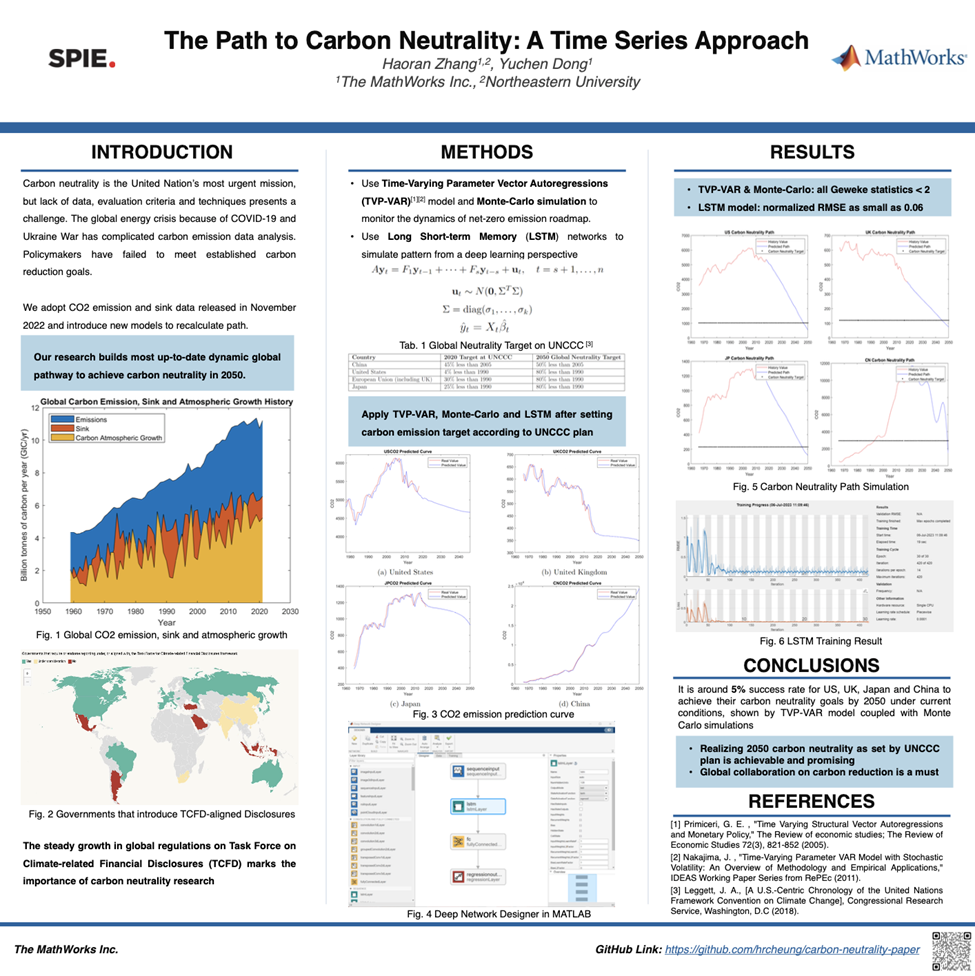

The Path to Carbon Neutrality: A Time Series Approach

The following blog was written by Leslie Zhang, a Northeastern graduate who recently joined MathWorks Engineering...

más de 1 año hace

Publicado

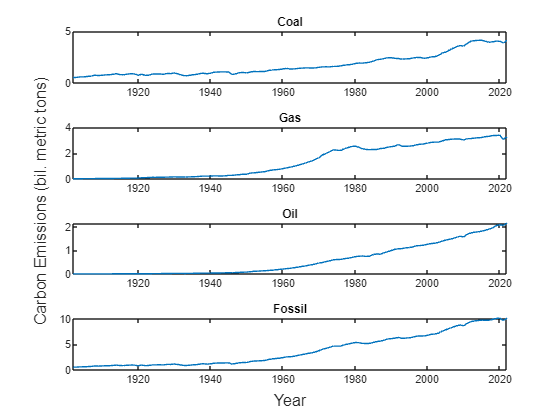

Time Series Analysis of Trends in Global Carbon Emissions from Fossil Fuels

The following post is from Hang Qian, Software Developer on the Econometrics Toolbox Team. Global carbon emissions have...

más de 1 año hace

Publicado

MathWorks Finance Conference 2023

It’s my pleasure to give everyone a sneak peek into the upcoming MathWorks Finance 2023 conference, which will be held...

más de 1 año hace

Publicado

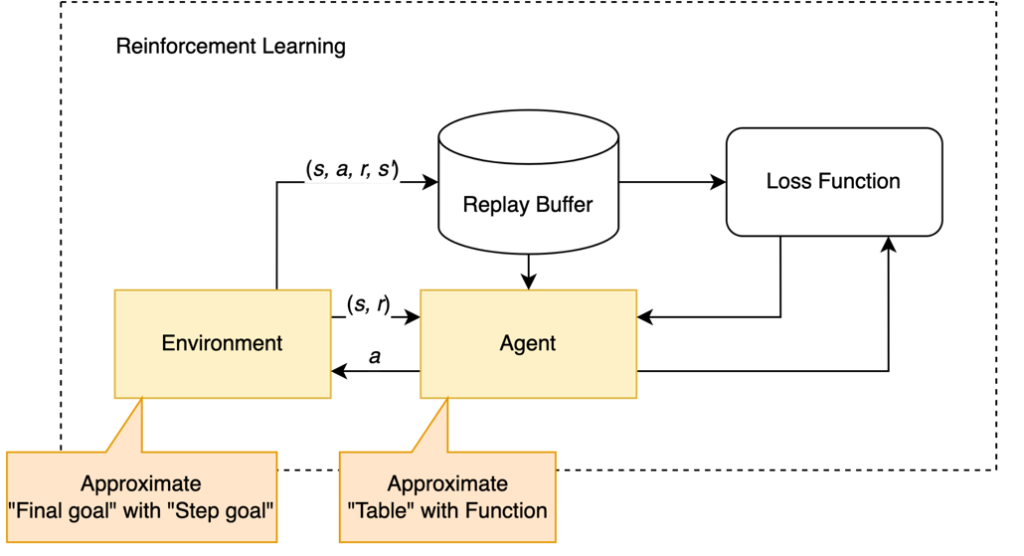

Reinforcement Learning as your portfolio advisor

The following post is from Ian Chie, Bowen Fang, Botao Zhang and Yichen Yao from Columbia University. Inspiration Let’s say...

más de 1 año hace

Publicado

Quantum Computing for Optimizing Investment Portfolios

The following post is from Sofia Ma, Senior Engineer for Finance Quantum computing is a cutting-edge field of study that...

más de 1 año hace

Publicado

The evolution of Quantitative Finance in MATLAB (What’s New)

Hi Everyone, I would like to welcome you to our new blog on Quantitative Finance. To kick things off, I’d like to give an...

casi 2 años hace

Seleccione un país/idioma

Seleccione un país/idioma para obtener contenido traducido, si está disponible, y ver eventos y ofertas de productos y servicios locales. Según su ubicación geográfica, recomendamos que seleccione: United States.

También puede seleccionar uno de estos países/idiomas:

América

- América Latina (Español)

- Canada (English)

- United States (English)

Europa

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)