Conditional Variance Models

Conditional variance models attempt to address volatility clustering in univariate time series models to improve parameter estimates and forecast accuracy. To model volatility, Econometrics Toolbox™ supports the standard generalized autoregressive conditional heteroscedastic (ARCH/GARCH) model, the exponential GARCH (EGARCH) model, and the Glosten, Jagannathan, and Runkle (GJR) model.

To convert from the previous conditional variance model analysis syntaxes, see Converting from GARCH Functions to Model Objects.

Conditional Variance Model Basics

Categories

- GARCH Model

Generalized, autoregressive, conditional heteroscedasticity models for volatility clustering

- EGARCH Model

Exponential, generalized, autoregressive, conditional heteroscedasticity models for volatility clustering

- GJR Model

Glosten-Jagannathan-Runkle GARCH model for volatility clustering

Featured Examples

Model Exchange Rate Volatility

Model exchange rate volatility using a GARCH model.

Compare Conditional Variance Models Using Information Criteria

Compare the fits of several conditional variance models using AIC and BIC.

Using Bootstrapping and Filtered Historical Simulation to Evaluate Market Risk

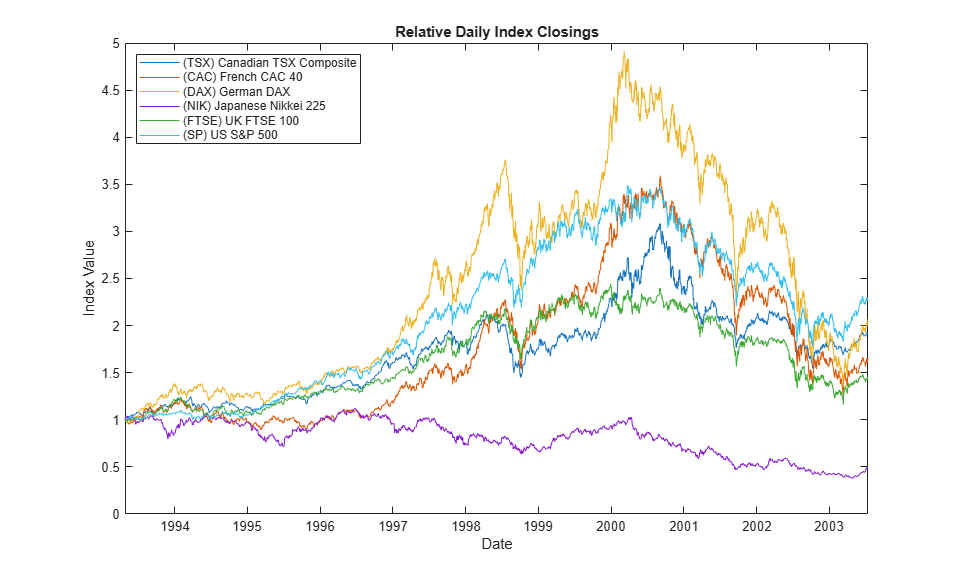

Assess the market risk of a hypothetical global equity index portfolio using a filtered historical simulation (FHS) technique, an alternative to traditional historical simulation and Monte Carlo simulation approaches. FHS combines a relatively sophisticated model-based treatment of volatility (GARCH) with a nonparametric specification of the probability distribution of assets returns. One of the appealing features of FHS is its ability to generate relatively large deviations (losses and gains) not found in the original portfolio return series.

Using Extreme Value Theory and Copulas to Evaluate Market Risk

Model the market risk of a hypothetical global equity index portfolio with a Monte Carlo simulation technique using a Student's t copula and Extreme Value Theory (EVT). The process first extracts the filtered residuals from each return series with an asymmetric GARCH model, then constructs the sample marginal cumulative distribution function (CDF) of each asset using a Gaussian kernel estimate for the interior and a generalized Pareto distribution (GPD) estimate for the upper and lower tails. A Student's t copula is then fit to the data and used to induce correlation between the simulated residuals of each asset. Finally, the simulation assesses the Value-at-Risk (VaR) of the hypothetical global equity portfolio over a one month horizon.