Using Science-Based Targets to Temperature Score Financial Portfolios

Get an overview of how to use MATLAB® with the Science Based Targets initiative (SBTi), which enables companies to reduce emissions in line with the Paris Agreement goals.

With the help of a simple app in MATLAB, end users can understand the temperature contribution, or the carbon coverage, of their financial equity portfolios.

Learn more about using MATLAB for climate finance, in this case, modeling temperature contribution of portfolios.

Published: 18 Oct 2021

Hello, and welcome to this presentation on responsible investing. A typical portfolio construction exercise has an objective of maximizing or minimizing a given metric. Some examples are Sharpe ratio, or variance. Yet another metric that one could think of minimizing is the temperature score of a portfolio. That's a proxy for contribution of the portfolio to temperature, global warming.

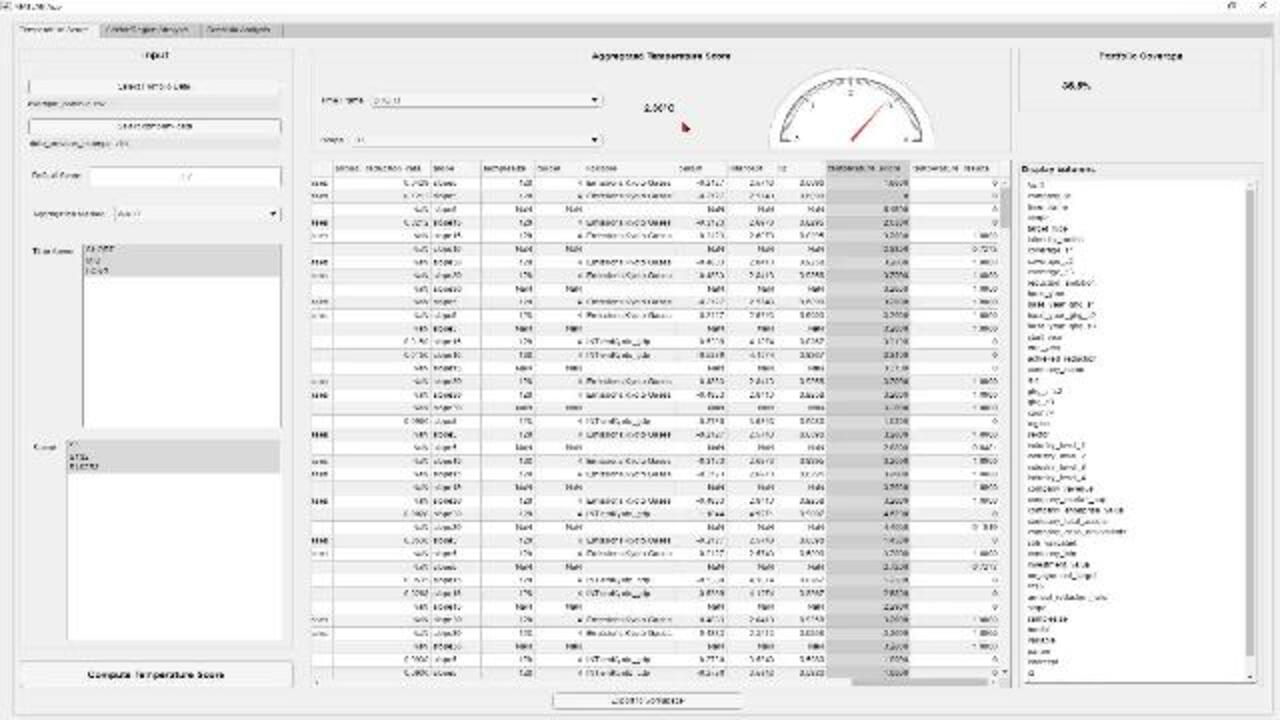

Here's an app that uses data on portfolio and the greenhouse gas emissions to calculate the temperature score of a portfolio. Using the methodology outlined by the Carbon Disclosure Project and the science based targets initiative, we calculate the temperature score of each of these stocks in the portfolio and the resulting temperature score of the portfolio.

Let's switch over to MATLAB, to the presentation. Let's switch over to the presentation. What are some typical challenges that people face when performing portfolio optimization? They need access to robust code for portfolio construction, optimization, and backtesting. While conducting portfolio optimization, or portfolio construction, people are building heterogeneous strategies with different rebalancing frequencies.

Backtesting them is an involved task, and you need to be able to minimize human error while working with lots of strategies. MATLAB facilitates this task by providing access to portfolio object and also the backtesting framework. Let's quickly switch over to MATLAB.

So here, I've set up a portfolio construction exercise. I'm reading in the data over here. I'm building portfolio using very few lines of code. And I've also calculated the max Sharpe ratio over here, and plotted the same using these lines of command. Now, I have created a simple backtesting strategy. And I'm running the backtest over here. After constructing this strategy, I could leverage the backtesting engine, run backtest and summary, for creating a quick summary of my backtest, and observing the characteristics of my portfolio.

Using the equity curve, I can have the evolution of my portfolio plotted, quickly. As you can see over here, I'm using the portfolio object. As you can see here. So this is a class that has been defined in MATLAB. And I'm going to use this class to add another method to minimize the temperature score. So I've created another class called temperature score, which inherits from the portfolio class.

I'm taking in some data over here. And I've added a new method that minimizes the temperature scope. So an example would be-- so I start with a returns metrics, calculate the mean, covariance, and I create my object, which is the temperature score. s And then I'm able to calculate the method, minimize temperature score, and that gives me the weight for each of the stocks in my portfolio. That minimizes the temperature score of the portfolio.

So as you can see, MATLAB gives me access to robust code. And with minimal effort, I'm able to extend my logic for portfolio construction. And I'm able to add another method to minimize the temperature score of my portfolio. Let's switch over to the presentation.

So we saw one way, one set of data, that we could use to minimize temperature score, which is the data from SVTI, that we could use to calculate the temperature score of the portfolio. So going back into the app, we saw how we could use the portfolio data and the company level greenhouse gas emission data to calculate the temperature score of the portfolio.

Now, we could extend this analysis to look at how each sector or region contributes to the temperature score. So here we have a temperature score that's split by regions. And here we have the same, but split across sectors as well, to have a quick glance into how each sector does in terms of minimizing the contribution to temperature score.

There's also provision to perform scenario analysis, where if we were to convince the stocks, or have stocks that commit to the approved as BK targets, we'll be able to minimize the temperature scope of each of these stocks in our portfolio to something lower. So let's see. For example, we set the scenario to approve targets, add scenario, and we see that the temperature score of portfolio is lower than to two degrees centigrade.

So we saw some challenges, which was to have access to robust code for portfolio construction and backtesting. We saw some heterogenous strategies that were implemented. And while constructing these heterogenous strategies, there is a possibility of having different rebalancing frequencies.

We also saw how another challenge of portfolio construction exercise is to minimize human error. We saw, as a way of addressing this challenge, how in MATLAB we have access to tested code for portfolio construction. We have a built-in backtesting framework. And we're able to access data from a diverse set of data sources, visualize them, and work with them intuitively in MATLAB. This brings us to the end of my presentation. Thank you for your time. Happy to take your questions.

Featured Product

MATLAB

Seleccione un país/idioma

Seleccione un país/idioma para obtener contenido traducido, si está disponible, y ver eventos y ofertas de productos y servicios locales. Según su ubicación geográfica, recomendamos que seleccione: United States.

También puede seleccionar uno de estos países/idiomas:

América

- América Latina (Español)

- Canada (English)

- United States (English)

Europa

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)