MATLAB para finanzas cuantitativas y

gestión de riesgos

Utilice MATLAB para importar datos, desarrollar algoritmos, depurar código, aumentar la potencia de procesamiento, etc.

Utilice MATLAB para importar datos, desarrollar algoritmos, depurar código, aumentar la potencia de procesamiento, etc.

Con unas pocas líneas de código de MATLAB, es posible prototipar y validar modelos financieros computacionales, acelerar esos modelos mediante el procesamiento paralelo e integrarlos directamente en la producción.

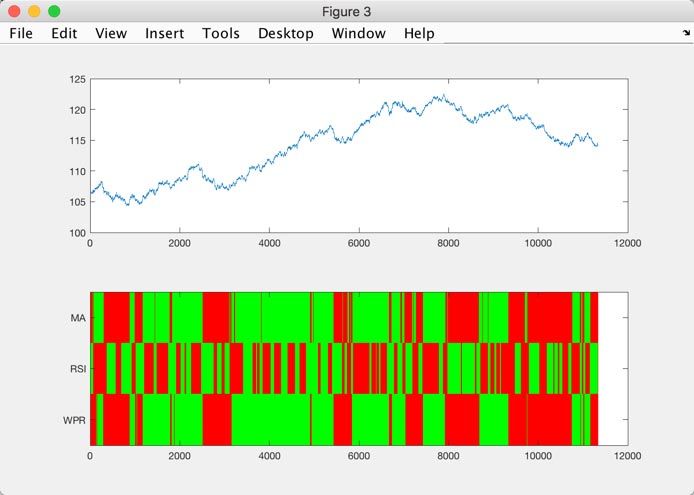

Instituciones de primer orden emplean MATLAB para determinar los tipos de interés, realizar pruebas de stress, gestionar carteras de varios miles de millones de dólares y llevar a cabo el trading de instrumentos complejos en menos de un segundo.

“MATLAB nos ha permitido concentrarnos en nuestras funciones básicas como profesionales de la inversión y desplegar un panel de optimización de carteras y gestión de riesgos cuantitativos que ha añadido valor desde el primer día para todo el equipo.”

Mathew John y Jason Liddle, SMMI

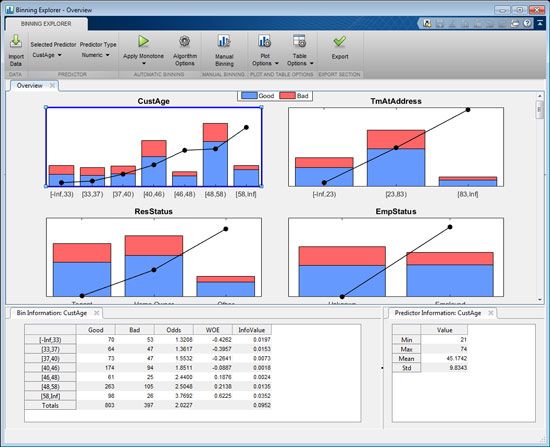

Gestión del riesgo de modelos financieros

Controle, desarrolle, valide, implemente y supervise modelos de diferentes líneas de negocio

Vea el progreso en productos de energía limpia, investigación climática y riesgo financiero y sostenibilidad.

Más información

Explore casos de éxito de los clientes:

Explorar productos

Explore casos de éxito de los clientes:

Más información

Explorar productos

Explorar productos

30 días de exploración a su alcance

Más información

Guía práctica: modelado del riesgo financiero con MATLAB

Lea el e-bookTambién puede seleccionar uno de estos países/idiomas:

América

Europa

Asia-Pacífico